Summary

The stalled budget reconciliation bill replaces the Additional Child Tax Credit (ACTC), which paid cash to low-income workers with children, with a program that is part of the enhanced Child Tax Credit (CTC). The program resembles traditional cash welfare because it entirely drops the old ACTC’s work requirement. It also significantly increases payment size. The new program was authorized in the stimulus for one year. As was true of the old ACTC, any illegal immigrant with a U.S.-born child is eligible for the new program. We estimate that illegal immigrants will receive $8.2 billion in payments from the new program annually — more than triple what they were eligible for under the old ACTC — while legal immigrants will receive $17.2 billion. The 10-year cost just for illegal immigrants would total roughly $80 billion.

If passed, the new program has profound implications for the immigration debate because it now means that the arrival of any low-income immigrant (legal or illegal) who has a U.S.-born child will have a much larger negative fiscal impact than was previously the case. The new cash payments for low-income parents should not be confused with the advance refunds many parents who pay federal income tax began receiving in July 2021. While the new CTC also provides payments starting in July, the program is for parents who do not pay federal income tax. It is not a tax refund, even though it is sometimes referred to as a “refundable tax credit”.

Among the findings:

- Based on their income and number of dependents, we estimate that 63 percent of all immigrant-headed families (legal and illegal) with children will receive the new cash grant — 57 percent for legal immigrants and 79 percent for illegal immigrants. In comparison, 52 percent of native families with children will receive payments.

- Legal and illegal immigrant parents who qualify for the program are eligible for somewhat larger payments on average than the native-born — about $5,100 for illegal immigrants and $4,800 for legal immigrants. This compares to about $4,600 for the native-born.

- The larger share of immigrants with children accessing the program and the more generous payments they will receive primarily reflect their lower average incomes.

- We estimate that all immigrants (legal and illegal) will receive $25.4 billion from the new program annually, accounting for 27 percent of its total costs, with legal immigrants receiving $17.2 billion, and illegal immigrants receiving $8.2 billion.

- Though a larger percentage of illegal immigrants are poor and qualify for the new program, the total amount paid out to legal immigrants is much larger because there are more low-income legal immigrants in the country.

- Relative to the old ACTC, illegal immigrants with children will be receiving larger payments not only because the program is much more generous for everyone, but also because the old work requirements made it difficult for some illegal immigrants who worked off the books to demonstrate employment. Dropping the work requirement makes it easier for all illegal immigrants with U.S.-born children to access the new program, even those who do not work.

Introduction

Possibly the biggest initiative undertaken by the Biden administration to assist low-income families is the enhanced Child Tax Credit (CTC). The new program was passed as part of the American Rescue Plan, signed by the president in March 2021. The stalled budget reconciliation bill, sometimes called the “safety net” bill, seeks to make the enhanced CTC permanent. At the time of publication, it is unknown if the new program will be modified in order to secure its passage as part of the budget reconciliation. As presently constructed, the program is both a large tax cut for families with children who pay federal income tax and a dramatic increase in cash benefits for those who do not pay income tax. The New York Times wrote that the new program, if implemented, has “the makings of a policy revolution”.

The new cash program replaces the old Additional Child Tax Credit (ACTC) and is sometimes referred to as a “child allowance” or even the new ACTC or just new Child Tax Credit (CTC). In this article, we will refer to it as the “new CTC” to distinguish it from the “old ACTC”. The maximum cash grant, which is referred to as a “refundable credit”, is more than twice the size of the old ACTC. This is potentially revolutionary because the payments are so large that proponents hope it will substantially reduce child poverty. It is also seen as revolutionary by critics because, by dropping any work requirement, the new CTC effectively undoes a central tenet of the 1996 welfare reform.

Like the old ACTC, for a parent to receive the new cash payment, only their dependent child(ren) needs to have a valid Social Security number (SSN), which all persons born in the United States receive. The parent does not need a valid SSN. This means that anyone — legal permanent residents, long-term temporary visitors (e.g. guestworkers and foreign students), and illegal immigrants who have at least one U.S.-born child — can receive cash payments from the program if their income is low enough.

It has long been known that less-educated, low-income immigrants (legal or illegal) are a net fiscal drain on average. The large cash grants from the new CTC make that drain even larger. This has important implications for the immigration debate because it now means that the arrival of any low-income legal or illegal immigrant has a much larger potential negative fiscal impact than was previously the case.

We use the terms “immigrant” and “foreign-born” synonymously in this article to mean all persons who were not U.S. citizens at birth. They include naturalized citizens, permanent residents, and the smaller number of long-term, temporary visitors such as foreign students, guestworkers, and illegal (unauthorized) immigrants. We also use the terms “native”, “native-born”, and “U.S.-born” interchangeably to mean anyone who was a U.S. citizen at birth. The purpose of this analysis is to estimate how much foreign-born beneficiaries will receive in cash payments from the new CTC by legal status.

How the New Cash Grants Work

A Substantial Increase in Cash Grants. The new CTC reduces tax liability by $3,600 for children under six and $3,000 for children ages six to 17. If the value of the new credit is more than a family’s federal income tax liability, the family can receive a “refundable credit”, which is a cash grant. The maximum cash payment under the new program for those without federal income tax liability is the same as the reduction in tax liability — $3,600 for children under age six and $3,000 for children six to 17. This is substantially larger than the $1,400 maximum cash payment per child under the old ACTC. The Congressional Budget Office has estimated the new cash grants, excluding the refunds, will cost the federal treasury $66.2 billion above the $28.9 billion that the old grants cost, for a total cost of about $95 billion annually.1 The idea behind the old ACTC and the new enhanced CTC is that it provides tax relief for higher-income parents who have tax liability, while providing cash grants for parents who do not pay federal income taxes, with the goal of lifting more children out of poverty.

No Work Requirement for the New CTC. In addition to providing much more money, the new CTC drops the work requirements of the old ACTC. Under the old ACTC, those receiving cash payments had to show they earned at least $2,500 a year and the size of the cash payment could not exceed 15 percent of earnings above $2,500. Both of these requirements have been eliminated. For low-income people, the link to earnings in the old program meant that the more someone earned, the larger the payment they received from the program, at least up to a point. The new program has no such incentive, as the full value of the cash benefit is available to any low-income person with a child, including those who do not work at all, making it like traditional cash welfare.

The new cash grants from the CTC are paid in monthly installments that total half of what the beneficiary can expect to receive from the program once they file their taxes. This, too, makes it even more like traditional cash welfare, as beneficiaries do not have to wait until they file their taxes to get a check each month.

Illegal Immigrants Are Allowed to Receive the New CTC. As already noted, any person in the United States who has a dependent child with a valid Social Security number may receive cash from the new program. The child’s SSN must be “one that is valid for employment”. This is the type of SSN all persons born in the United States receive. If a child does not have an SSN, the tax filer cannot use the child to claim the credit or the cash grant. However, in its instructions for aliens (Publication 519), the IRS states that for a parent to receive the ACTC he or she needs either a SSN or an Individual Taxpayer Identification Number (ITIN). This is also stated on the IRS website. These are the same rules governing the new CTC. This means illegal immigrants with U.S.-born children can receive the new cash grants by getting an ITIN if they do not have an SSN, which millions already have.2 Relative to the old ACTC, illegal immigrants with children will be receiving much larger payments not only because the program is much more generous for everyone, but also because the old work requirements were difficult to demonstrate for some illegals who worked off the books.

Findings

Families with Children. Figure 1 shows that a larger share of immigrant families with children will receive cash payments from the new program than the native-born. Only parents with children under age 18 are eligible for cash from the new program. Still, it is striking that 78.8 percent of illegal immigrant families with children will receive cash from the new CTC. At 57.4 percent, the rate for legal immigrant parents is also quite high. The rate for the native-born is 51.8 percent. Clearly, the new program covers a very large share of children in America.

|

Why Immigrants Benefit More from the New CTC. Cash payments under the new CTC are mostly limited to families with income below 350 percent of poverty. For a family of three in 2020, this would be about $76,000. Using the 2019 and 2020 Census Bureau data, we find that 93 percent of families with children receiving cash from the new CTC have incomes below this level. Of all families with children headed by a foreign-born person, 66 percent have incomes below 350 percent of poverty — 60 percent for legal immigrants and 83 percent for illegal immigrants. Among native families with children, 53 percent have incomes this low. Thus, the larger share of immigrants who have children and lower incomes explains why they are more likely to benefit from the new cash program.

The primary reason immigrants have lower incomes is that they generally have lower levels of education. Looking at heads of illegal-immigrant families with children, we estimate that 46 percent have not graduated high school, compared to 16 percent of legal immigrant family heads. In comparison, only about 5 percent of native families with children are headed by a person without a high school education. Language and cultural factors also contribute to immigrants’ lower earnings. It is not the case that immigrants’ lower incomes are caused by not working, as immigrants with children are at least as likely to work as the native-born.

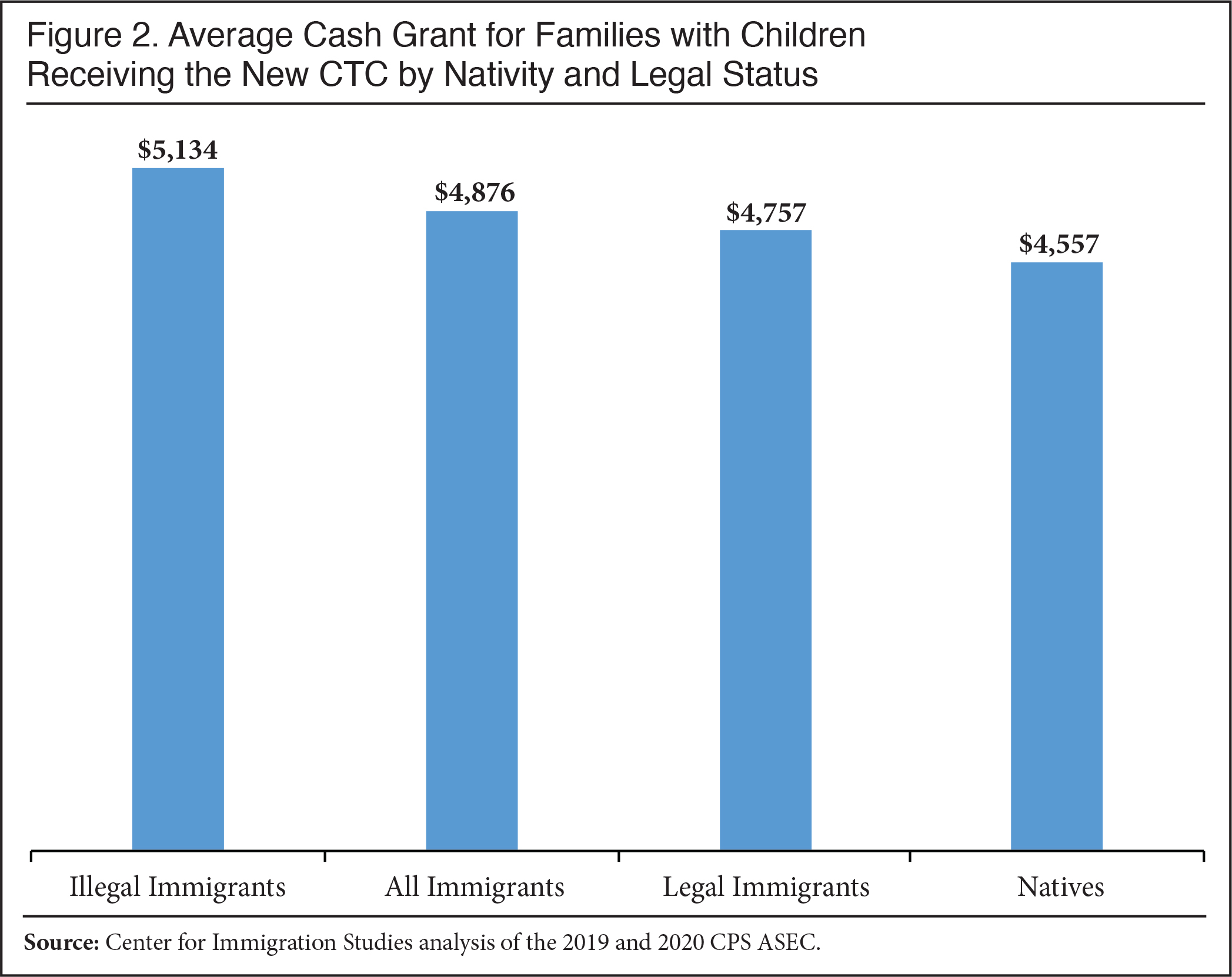

Average Cash Payment. Figure 2 shows the average payment size for families receiving cash from the new CTC. The figure shows that legal and illegal immigrant parents who qualify for the program are eligible for somewhat larger payments on average than the native-born — $5,134 for illegal immigrants and $4,757 for legal immigrants. This compares to $4,557 for the native-born. The larger payments under the new program that immigrants will receive mainly reflect their lower incomes and slightly larger families.

|

Total Cost of the Program. Based on the 2019 and 2020 Current Population Survey’s Annual Social and Economic Supplement (CPS ASEC), we estimate that the total annual cost of the program as currently constructed will be $95.7 billion. This is in line with the Congressional Budget Office’s estimate of the program’s total expected costs of about $95 billion. Immigrants as a whole will receive $25.4 billion from the new program annually — $17.2 billion for families headed by legal immigrants and $8.2 billion for those headed by illegal immigrants. We have previously estimated that illegal immigrants may have received $2.5 billion from the old ACTC. The new CTC roughly triples what illegal immigrants will receive. Projections over time are dependent on the size of the relevant population, but assuming a static illegal immigrant population with stable characteristics, then the 10-year cost of the new program just for illegal immigrants could total $80 billion.

Conclusion

The new CTC represents a profound change in social policy. On one hand, it may help significantly reduce child poverty, but it may also significantly undermine work incentives. As for immigration, the decision to allow illegal immigrants with U.S.-born children to receive the new program means that those in the country without authorization will be receiving large cash payments from American taxpayers. Further, choosing to allow illegal immigrants to receive these cash grants seems likely to encourage more illegal immigration.

While encouraging illegal immigration seems unwise, perhaps the biggest implication for immigration of the new program is that, if passed, the arrival of any low-income immigrant (legal permanent resident, guestworker, or illegal alien) has a much more negative fiscal impact than was previously the case. There has always been a concern that allowing in less-educated immigrants to fill low-wage jobs, while popular with employers, has a negative impact on public coffers. Low-wage workers, immigrant or U.S.-born, by design pay relatively little in taxes, while they or their children are often eligible for a host of social programs. Creating a new large new benefit will only add to the net fiscal costs. Backers of the new CTC do not seem to have considered the implications of such a program for immigration policy.

Methodology

Data Source. Our analysis is based on the 2019 and 2020 CPS ASEC collected in March each year by the Census Bureau for the Bureau of Labor Statistics. The survey asks respondents about their income from all sources and the relationship of each person in the household. With this and other information, the Census Bureau identifies the primary tax filer or filers in each household and all the dependents linked to that person. The Census Bureau then calculates federal income tax liability for each primary filer before any cash credits are received. Even adults with little or no income can be tax filers if defined in this way.

Estimating Tax Liability and CTC Grants. Because the Census Bureau has calculated the tax liability for all respondents to the CPS ASEC, it is a relatively straightforward matter to calculate what families are likely to receive in cash from the enhanced CTC by subtracting from their liability $3,600 for each child under six and $3,000 for each child ages six through 17. Because the dependent(s) must have a valid SSN, we exclude the roughly 15 percent of dependent children who are illegal immigrants from the analysis.

Illegal Immigrants. It is well established that those in the country illegally are present in Census data, but they are never explicitly identified by the bureau. To determine which respondents are most likely to be illegal aliens, we first exclude immigrant respondents who are almost certainly not illegal aliens — for example, spouses of native-born citizens; veterans; people who receive direct welfare payments; people who have government jobs; Cubans (because of special rules for that country); immigrants who arrived before 1980 (because the 1986 amnesty should have already covered them); people in certain occupations requiring licensing, screening, or a government background check (e.g., doctors, pharmacists, and law enforcement); and people likely to be on student visas.

The remaining candidates are weighted to replicate known characteristics of the illegal population (population size, age, gender, region or country of origin, state of residence, and length of residence in the United States). CIS has previously used the Department of Homeland Security (DHS) as the source of those known characteristics; however, DHS’s most recent estimates are for 2018. For 2019 data, we turn to estimates from the Center for Migration Studies (CMS). The resulting illegal population, which consists of a weighted set of CPS ASEC respondents, is designed to match CMS on the additional characteristic of education.

End Notes

1 The Congressional Budget Office estimates that additional costs from the program for 2021 will be $66.185 billion. See p. 25 in “Congressional Budget Office Cost Estimate”, revised February 17, 2021. The existing cost of the replaced ACTC was $28.898 billion. See p. 1029 in “A Budget for America’s Future, Appendix”.

2 It is not certain how many illegal immigrants are using ITINs to receive tax refunds, “refundable credits”, and cash payments because the government has not published the number of tax filers who used ITINs since 2015, when 4.35 million reportedly used them to file. The 2015 “National Taxpayer Advocate Report to Congress” shows the most recent information on ITINs, starting on p. 198. Strangely, the 2016 report cites the ITIN figures from the 2015 report (footnote 2, p. 239), but contains no updated numbers. No Advocate’s reports after 2016 have updated ITIN figures. Further, the most recent Treasury Inspector General for Tax Administration’s report on problems with ITINs also does not report how many people are using them in recent tax years.