Download a PDF of this Backgrounder.

Jason Richwine is a resident scholar at the Center for Immigration Studies.

Summary

Under current law, illegal immigrants are net contributors to Social Security and Medicare. They partially pay in to entitlement programs, but cannot legally receive benefits. By granting eligibility for benefits, however, amnesty would transform illegal immigrants from net contributors into net beneficiaries, imposing steep costs on the Social Security and Medicare trust funds:

- Amnesty would impose a lifetime net cost on Social Security and Medicare Part A (hospital insurance) of about $129,000 per amnesty recipient. This cost is the present discounted value of benefits received minus new taxes paid.

- If 10 million illegal immigrants receive amnesty, the total cost to Social Security and Medicare Part A would be roughly $1.3 trillion in present value, equivalent to a one-time transfer of 6 percent of GDP.

- Because most of these costs would occur outside its 10-year budget window, the Congressional Budget Office is unlikely to include them when it scores amnesty legislation.

Introduction

Congress may consider several bills this year that would offer legal status and a path to citizenship to illegal immigrants.1 Although amnesty would have wide-ranging legal and political effects, this report focuses on the most salient fiscal effect – namely, the added costs to Social Security and Medicare.

Amnesty is costly to Social Security and Medicare for two main reasons. First, both programs have a progressive benefit structure, meaning that lower-income participants receive more benefits relative to their contributions compared to high earners. In the case of Social Security, participants contribute the same 12.4 percent tax on all earnings up to the maximum taxable salary, but their benefits increase at a slower rate as their earnings increase. Medicare is even more progressive because it hardly depends on earnings at all. Once participants have worked for 10 years at a minimal earnings level, they become eligible for the same benefits as high-earning, full-career workers. Because illegal immigrants tend to have lower earnings and work fewer years in the U.S. than the average Social Security and Medicare participant, as a group they will benefit from these programs’ progressive benefit structures — if, that is, they become eligible through amnesty.

A second reason that amnesty would be costly to Social Security and Medicare is that many illegal immigrants are currently paying into the system without accruing any benefits in return. Although the exact percentage is unknown, roughly half of illegal immigrants are thought to be contributing payroll taxes — either because they entered a fake Social Security number (SSN) on employment forms, or because they acquired a real SSN through former legal status or fraud.2 The “free” contributions made by these taxpaying illegal immigrants are a fiscal positive for the U.S., but amnesty would reverse the situation. Once illegal immigrants receive amnesty and become eligible for Social Security and Medicare, they will no longer be net contributors who partially pay in without receiving anything in return. Instead, they will become net beneficiaries who receive more in benefits than they contribute in taxes. It is this dramatic change in status that makes amnesty so costly to the system.

This report estimates amnesty’s impact on Social Security and Medicare by comparing the new cost to the status quo in which illegal immigrants continue to work in the U.S. without authorization. In order to contain the analysis to programs funded through the payroll tax, this report considers only Social Security and Medicare Part A (hospital insurance). Although amnesty is surely costly to Medicare Part B (outpatient care) and Part D (prescription drugs), those programs are funded through general revenue, and including them would require a much broader analysis.

For more on how the analysis was conducted, see “Detailed Methods” at the end of this report. Please note that although the analysis is thorough, it still requires several simplifying assumptions. The estimates it produces are just that — estimates, not exact figures. Furthermore, this report considers only the impact of amnesty as it compares to the status quo – in other words, it takes the presence of illegal immigrants as a starting point and then analyzes the cost of granting them amnesty. The more general issue of how newly arriving immigrants affect entitlements is not addressed here. Finally, the question of whether taxpaying illegal immigrants “deserve” to receive entitlement benefits is distinct from the question of how costly such a policy change would be. See the “Discussion” section for more on this point.

Results

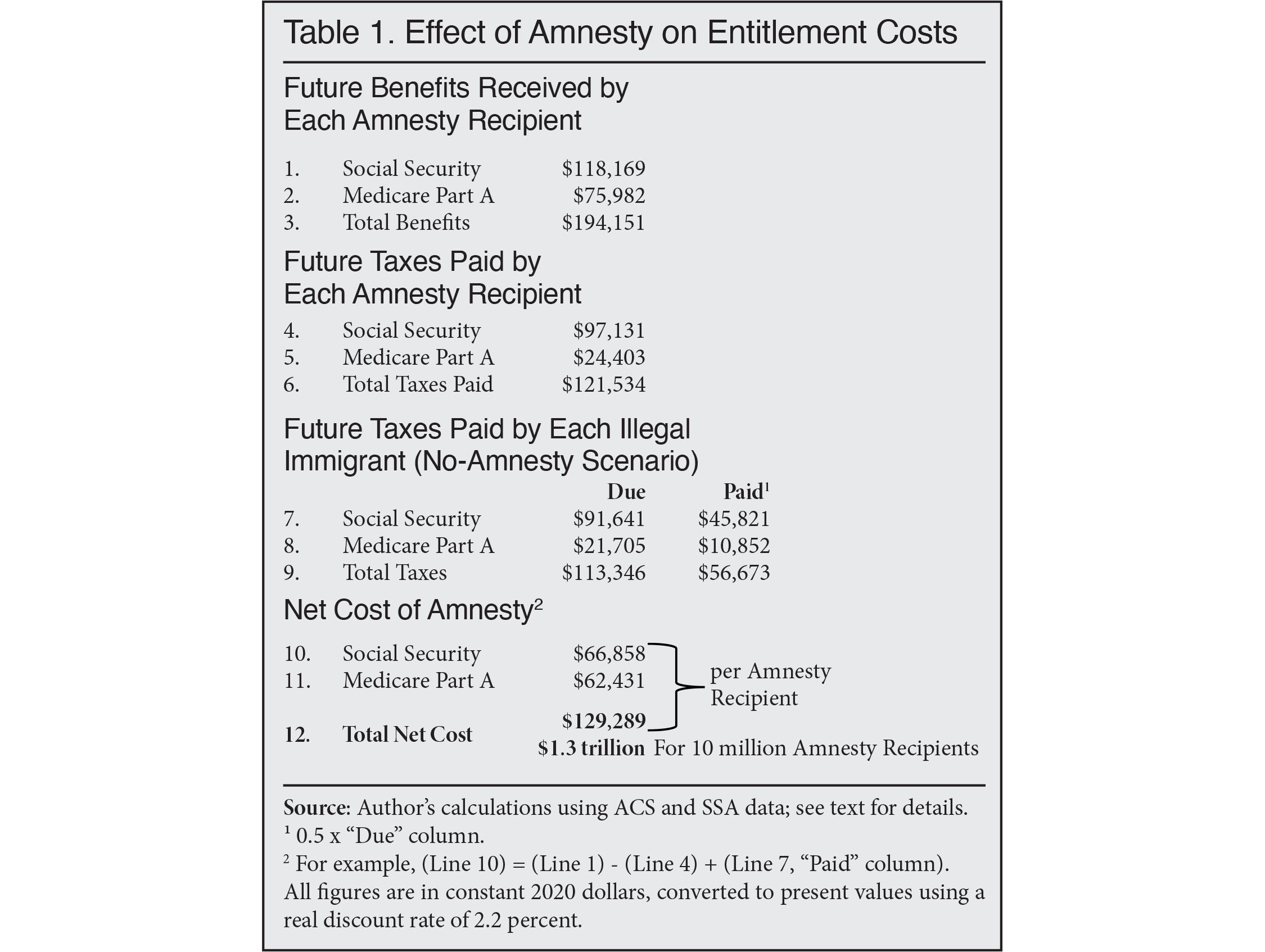

The table below has four major sections. The first section shows the benefits that each amnesty recipient will likely receive. For example, Line 1 indicates that the average amnesty recipient is predicted to receive $118,169 in lifetime Social Security benefits.

|

The next two sections compare the taxes paid by illegal immigrants in the amnesty and no-amnesty scenarios. Line 5 indicates that the average amnesty recipient will pay $24,403 in future contributions to the Medicare Part A trust fund. By contrast, if illegal immigrants do not receive amnesty, they will owe $21,705 in Medicare taxes (Line 8, “Due” column). They will owe less than in the amnesty scenario because their incomes are not as high. Furthermore, without amnesty, only 50 percent of illegal immigrants can be expected to actually pay the taxes they owe. Therefore, the Medicare taxes paid by the average illegal immigrant are $10,852 (Line 8, “Paid” column).

The fourth section displays net costs. The total net cost on Line 12 is simply the total benefits (line 3) minus the new taxes paid due to amnesty. The amount of new taxes paid is the difference between tax payments in the amnesty and non-amnesty scenarios (Line 6 minus the “Paid” column of Line 9). At a net per-recipient cost of $129,289, amnesty appears to be quite expensive.

If 10 million illegal immigrants were to receive amnesty, the total cost to taxpayers would be $1.3 trillion. If such a large amnesty seems unlikely, however, then one can approximate the impact of a smaller amnesty by multiplying the expected number of recipients by the per-recipient cost on Line 12.3 Similarly, if readers do not believe that the fraction of illegal immigrants who contribute payroll taxes is 50 percent, they can multiply the “Due” column in the no-amnesty scenario by their preferred percentage to compute the “Paid” column, then re-calculate net costs by following the formula given above.

Importantly, all of the costs listed in Table 1 are in “present value” terms. When financial analysts compare cash flows that occur over many years — as with periodic Social Security checks, for example — they “discount” future payments to reflect what they would be worth in the present. To illustrate using a 2.2 percent discount rate, $100 paid next year would be worth only $100/(1.022) = $97.85 today, and $100 paid two years from now would be worth $100/(1.022)^2 = $95.74 today. A present value converts a long stream of future payments into a single upfront cost. In this case, an amnesty for 10 million illegal immigrants would impose the equivalent of an immediate one-time cost of $1.3 trillion on American taxpayers. The actual payments would, of course, be distributed piecemeal over many years, and the simple sum of those payments (without discounting) would be much more than $1.3 trillion.

Discussion

Based on a set of plausible assumptions, this report estimates that amnesty will confer about $129,000 in net entitlement benefits to each amnesty recipient, implying a $1.3 trillion cost if the amnesty covers 10 million illegal immigrants.

Unfortunately, the Congressional Budget Office usually projects budgetary impacts only 10 years into the future, meaning it will capture almost none of the Social Security and Medicare costs associated with amnesty. Costs falling outside of the 10-year budget window are no less real, however. Lawmakers need to be aware of the full, long-term costs of any amnesty legislation that comes up for debate.

The costs described here are driven by amnesty itself, not by immigration in general. Whether bringing more immigrants into the U.S. burdens entitlement programs is a complicated question that hinges on issues of fertility and long-term growth. In the context of amnesty vs. the status quo, however, the immigrants are already here — the only issue is whether the U.S. will decide to pay them Social Security and Medicare benefits that they otherwise would not receive.

One may object that some illegal immigrants “deserve” to collect entitlement benefits because they are paying into the system.4 Legally, however, they cannot collect, and the government’s baseline fiscal estimates assume they will not. It is important to at least acknowledge the added cost associated with making illegal immigrants eligible for entitlements, even if one prefers that policy change as a normative matter.

Furthermore, the ethical case for allowing illegal immigrants to collect benefits is not so obvious. Most illegal immigrants surely knew they would be ineligible for benefits if they crossed the border without authorization or overstayed their visas. They chose to do so anyway. Unless one believes that there is nothing at all objectionable about living in a foreign country illegally, then taxation-without-benefits could be considered part of a reasonable set of penalties for breaking the law.

Detailed Methods

This report addresses the following question: Compared to the status quo in which illegal immigrants continue to live and work in the U.S. without authorization, what would be the cost to the Social Security and Medicare Part A trust funds if illegal immigrants receive amnesty? The steps taken to answer the question are numbered and described below.

1. Formalize the Question. Let SS_Med equal the Social Security and Medicare benefits collected by amnesty recipients, t(w_amnesty0) equal the payroll taxes due on the wages that illegal immigrants will earn in the absence of amnesty, and t(w_amnesty1) equal the payroll taxes due on the wages of amnesty recipients. Note the assumption that w_amnesty1 > w_amnesty0 because of greater bargaining power and occupational mobility that workers have after they are legalized.

Status Quo Scenario: Illegal immigrants live and work in the U.S. with their families. Half pay Social Security and Medicare taxes, but they are not eligible to collect benefits. In this scenario, the taxpayer cost is negative, meaning a subsidy for taxpayers:

Taxpayer Cost = - 0.5 x t(w_amnesty0)

Amnesty Scenario: Formerly-illegal immigrants continue to live and work in the U.S. with their families. However, they now have higher wages due to legalization; they all pay Social Security and Medicare taxes; and all who meet the work requirements going forward will be eligible for benefits.

Taxpayer Cost = SS_Med – t(w_amnesty1)

The effect of amnesty is the cost under the status quo scenario subtracted from the cost under the amnesty scenario:

Effect of Amnesty on Taxpayer Cost = SS_Med – t(w_amnesty1) + 0.5 x t(w_amnesty0)

2. Make Simplifying Assumptions. Generating concrete numbers from the above formula requires simplifying assumptions. The first assumption is that amnesty recipients will begin collecting Social Security benefits at the normal retirement age of 67. Actuarial adjustments for early and late retirements are intended to produce similar lifetime benefits, so this assumption should have minimal impact.

A more consequential assumption is no credit for work performed prior to amnesty. Only post-amnesty earnings enter into this Social Security benefit calculation, even if recipients had long work histories prior to amnesty. If amnesty recipients are allowed to claim benefits based on pre-amnesty earnings, the cost to taxpayers would be greater than what is reported here, since a longer work history will lead to larger benefit payments.5

For the small number of illegal immigrants who receive amnesty at age 58 or older, the assumption is that they will not collect any benefits because they will not have at least 10 years of work experience before retirement. Similarly, Medicare starts for most people at age 65. If illegal immigrants receive amnesty at age 56 or 57, they will not receive Medicare benefits until age 66 or 67, respectively. If illegal immigrants receive amnesty at age 58 or older, the assumption is that they will never receive any benefits through Medicare.

This report does not attempt to measure the cost of Social Security DI (disability insurance), benefits for surviving family members, or Medicare for people under the age of 65.6

3. Establish Covered Earnings in Census Data. The primary dataset used in this report is the 2018 American Community Survey (ACS), an annual mini-census that contains demographic information on a large sample of U.S. residents. Although newer data would be preferable, the most recent information on illegal immigrants also comes from 2018 (see below). Constant 2020 dollars are used throughout the report.

Earnings are “covered” if they incur payroll taxes and accrue credit toward Social Security and Medicare benefits. Covered earnings are the sum of employed and self-employed earnings, of which some workers may have both.7 After inflating covered earnings to 2020 constant dollars, the earnings are capped at $137,700 (the 2020 level) for purposes of calculating Social Security taxes and benefits. The earnings remain uncapped when calculating Medicare taxes.

4. Identify Illegal Immigrants in Census Data. Prior research indicates that most illegal immigrants are included in Census data. To locate them in the ACS, this report uses a procedure that CIS has employed many times. The first step is to exclude immigrant respondents who are almost certainly not illegal — for example, spouses of native-born citizens; veterans; people who have government jobs; Cubans (because of special rules for that country); immigrants who arrived before 1980 (because the 1986 amnesty should have already covered them); people in certain occupations requiring licensing, screening, or a government background check (e.g., doctors, pharmacists, and law enforcement); and people likely to be on student visas.

The remaining candidates are weighted to replicate known characteristics of the illegal population (population size, age, gender, region or country of origin, state of residence, and length of residence in the United States). CIS has previously used the Department of Homeland Security (DHS) as the source of those known characteristics; however, the most recent DHS data cover 2015.8 For newer data, this report uses the 2018 estimates from the Center for Migration Studies (CMS), including their estimates of educational attainment.9 The resulting illegal population, which consists of a weighted set of ACS respondents, is designed to match CMS on the characteristics listed above.

This approach necessarily assumes that the illegal immigrant population has a demographic profile (age, sex, etc.) similar to the one it did in 2018. However, the sheer size of the illegal population is less important here because entitlement costs are calculated on a per-recipient basis. As noted above, readers can simply multiply the per-recipient costs by the number of illegal immigrants who are expected to receive amnesty.

5. Estimate Illegal Immigrant Earnings Across the Life Cycle. The ACS is a cross-sectional dataset, meaning it captures each worker’s earnings at only one point in time. To estimate future earnings, illegal immigrants are first grouped by sex, Hispanic status, three levels of education (less than high school, high school diploma, and a four-year degree or more), and five-year age groups spanning 16 through 66.10 The next step is to calculate average covered earnings for each of these groups. The result is the familiar “hump-shaped” life cycle of earnings, with increasing earnings throughout early to middle adulthood before falling as retirement approaches.

The assumption is that each amnesty recipient will have a stream of income that follows the life-cycle curve that matches his or her grouping by sex, Hispanic status, and education. However, if a new amnesty follows the precedent set by the 1986 amnesty, recipients will likely receive a boost to their wages as their bargaining power and mobility increase.11 Rather than apply a single markup across the board, this report gives amnesty recipients the average of illegal and legal earnings within their sex-Hispanic-education-age group. The result is an overall average earnings boost for amnesty recipients of about 7 percent, including average boosts of 3 percent, 8 percent, and 11 percent for dropouts, high school graduates, and college graduates, respectively.

6. Add Up Earnings. Before calculating cumulative earnings, the lifetime streams of income noted above need to be adjusted upward in another way. The Social Security Administration (SSA) assumes that real wages will rise over the next several decades by an average of 1.23 percent per year due to economic growth.12 That growth factor needs to be applied to each income stream based on the age of the amnesty recipient. For example, consider a 40-year-old illegal immigrant who receives amnesty this year. If the income stream for his sex-Hispanic-education group indicates that he will earn $30,000; $30,500; and $31,000 when he is ages 40, 41, and 42, respectively, then his adjusted stream would be $30,000; $30,500 x (1.0123); $31,000 x (1.0123)^2; and so on.

7. Calculate Taxes Paid. Payroll taxes are calculated in two separate ways. To calculate taxes paid by illegal immigrants post-amnesty — t(w_amnesty1) from Step 1 above — cumulative earnings from Step 6 are used, including the 7 percent average earnings boost due to amnesty. To calculate taxes owed by illegal immigrants under the status quo — t(w_amnesty0) from Step 1 above — cumulative earnings without the amnesty earnings boost are used.

In either case, workers owe 12.4 percent up to the earnings cap for Social Security and 2.9 percent on their uncapped earnings for Medicare Part A. These percentages reflect both the employer and employee contributions. The taxes are discounted at SSA’s long-term real interest rate of 2.2 percent.13

8. Determine Annual Benefits. Social Security benefits are calculated according to the standard “high-35” formula. Yearly covered earnings are first adjusted to match wage levels in the year the recipient turns 60, and then the highest 35 years are averaged together and divided by 12 to produce “average indexed monthly earnings”, or AIME.

The primary insurance amount (PIA) is 90 percent of the recipient’s AIME up to the first “bend point”, plus 32 percent of AIME between the first and second bend points, plus 15 percent of any AIME exceeding the second bend point. For workers who turn 62 in 2021, the first bend point is $996, and the second is $6,002. (Age 62 is the first year of retirement eligibility, but remember that this report assumes the normal retirement age of 67, for simplicity.)

For example, a worker who becomes eligible to retire in 2021 with an AIME of $7,000 would receive the following PIA:

0.9 x $996 + 0.32 x ($6,002 - 996) + 0.15 x ($7,000 - $6,002) = $2,648 per month

The assumption is that the bend points grow each year in line with the average real wage-growth of 1.23 percent mentioned in Step 6.

Finally, federal income taxes on Social Security benefits are credited to the Social Security and Medicare Part A trust funds, so those taxes should be subtracted from the total benefits calculated here. A 2015 paper from SSA estimates that about 10 percent of benefits will be owed as taxes over the next several decades.14 The tax is progressive, however, and amnesty recipients will have lower benefits than the average worker. This report uses a 5 percent tax rate as a more reasonable estimate for amnesty recipients.

Medicare is conceptually simpler, since benefits do not depend on wages once minimum eligibility rules are satisfied. The per-person cost of Medicare Part A in 2020 is $5,644, and the program’s trustees predict it will experience a real growth rate of 1.5 percent per year.15

9. Determine Lifetime Benefits. SSA publishes life expectancy estimates by age and sex.16 However, life expectancy also varies significantly by ethnicity. Based on separate data from the CDC, this report supplements the SSA estimates by increasing Hispanic life expectancy by 7 percent for those over the age of 21, and by 4.5 percent for those who are 21 or younger.17 With life expectancy established, lifetime benefits are simply the product of annual benefits and the number of receiving years. As with taxes, all benefits are discounted at 2.2 percent.

10. Compute the Final Cost. To determine the taxpayer cost of amnesty, the final step is to plug in the taxes and benefits to the formula given in Step 1.

End Notes

1 The Menendez bill pending in the Senate would grant amnesty to nearly all illegal immigrants who arrived before the start of this year. Supporters may also advance smaller measures, such as the Dream Act and the Promise Act. See Mark Krikorian, “Amnesty: Comprehensive or Piecemeal?”, National Review, February 18, 2021.

2 In reviewing some older research, the CBO noted that up to 75 percent of illegal immigrants file income tax returns. See “The Impact of Unauthorized Immigrants on the Budgets of State and Local Governments”, Congressional Budget Office, December 2007. However, many do so with an individual taxpayer identification number, not an SSN, so they may not be contributing payroll taxes.

The Social Security Administration has estimated that roughly half of illegal immigrant workers use some kind of SSN, valid or not. See Joel Feinleib and David Warner, “The Impact of Immigration on Social Security and the National Economy”, SSA Issue Brief #1, December 2005; and Stephen Goss, et. al., “Effects of Unauthorized Immigration on the Actuarial Status of the Social Security Trust Funds”, SSA Actuarial Note No. 151, April 2013.

It would be useful to have more recent estimates. Since visa overstays are an increasingly large source of illegal immigration, the proportion of illegal immigrants with SSNs has probably risen. See Robert Warren and Donald Kerwin, “The 2,000 Mile Wall in Search of a Purposs”, Journal on Migration and Human Security, Vol. 5, No. 1, pp. 124-136. In any case, the “Results” section of this report explains how readers can change the cost estimates themselves by substituting a different proportion who are currently paying into the system.

3 Changing the expected number of amnesty recipients may also be necessary to deal with special cases. For example, some illegal immigrants with stolen SSNs may actually be accruing benefits already — albeit not for themselves, but for the rightful owners of the SSNs.

Furthermore, recipients of Temporary Protected Status (TPS) and Deferred Action for Childhood Arrivals (DACA) can legally access Social Security and Medicare under their current status, so one must decide if these programs are truly temporary before including them among amnesty recipients in future legislation. See William R. Morton and Audrey Singer, “Social Security Benefits for Noncitizens”, Congressional Research Service, November 17, 2016.

Finally, some illegal immigrants may be able to acquire legal status through sponsorship by their U.S.-born children, then collect entitlement benefits without ever receiving a formal amnesty. In order for this to affect the analysis here, the sponsorship would have to occur before the parent reaches 58 years old, since this report assumes that legalization for people 58 or older does not impose any entitlement costs. The requirement that most illegal immigrants remain outside the country for 10 years before acquiring a green card is also a barrier, at least in theory.

4 Richard Alba, normally a careful scholar, once hyperbolically declared that withholding benefits from taxpaying illegal immigrants is “a morally bankrupt idea that amounts to endorsing payroll tax theft.” See “The Strange Math of the Heritage Foundation’s Immigration Report”, Democracy, May 17, 2013.

5 Unless amnesty legislation specifically bans the practice, recipients with previously valid Social Security numbers — e.g., visa overstayers — will probably be able to count their pre-amnesty earnings toward their benefits (Morton and Singer, 2016).

6 Under-65 individuals who are on Social Security DI or who have end-stage renal disease are generally eligible for Medicare.

7 Following IRS rules, self-employed earnings are multiplied by 0.9235 before being added to employed earnings.

8 “Estimates of the Unauthorized Immigrant Population Residing in the United States”, Department of Homeland Security, undated.

9 “State-Level Unauthorized Population and Eligible-to-Naturalize Estimates”, Center for Migration Studies, undated.

10 Illegal immigrants who are aged 22 or older are assumed to have completed their educations. For those under 22 (“young illegal immigrants”), this report assigns them the most common educational level held by older illegal immigrants with the same entry age and Hispanic status. As a result, most young illegal immigrants are coded as high school graduates. However, this method does produce a different result for those who entered in their late teens. Non-Hispanics in that entry-age group are designated as college graduates, while Hispanics in the same entry-age group are designated as dropouts.

11 Wages rise for amnesty recipients, but their employment rates decrease, resulting in a mixed effect on earnings. See Catalina Amuedo-Dorantes, Cynthia Bansak, and Steven Raphael, “Gender Differences in the Labor Market: Impact of IRCA’s Amnesty Provisions”, American Economic Review, Vol. 97, No. 2 (May 2007), pp. 412-416.

Taking both wages and employment levels into account, the Heritage Foundation assumed an across-the-board 5 percent earnings boost due to amnesty. (Robert Rector and Jason Richwine, “The Fiscal Cost of Unlawful Immigrants and Amnesty to the U.S. Taxpayer”, Heritage Foundation Special Report, May 6, 2013.) This report’s method produces a similar average earnings boost of 7 percent, but it improves on Heritage’s approach by varying the boost depending on demographic characteristics.

12 “2020 OASDI Trustees Report”, Social Security Administration, April 2020, Table V.B1.

13 More specifically, 2.2 percent is the average of the real yields on new bond issues predicted by SSA over the next 40 years (calculations from ibid., Table VI.G6).

14 Patrick J. Purcell, “Income Taxes on Social Security Benefits”, Social Security Administration, Issue Paper No. 2015-02, December 2015, Chart 2.

15 “2020 Medicare Trustees Report”, Centers for Medicare and Medicaid Services, April 2020, Table V.D1 and Table II.C1.

16 “Period Life Table”, Social Security Administration, 2017.

17 “United States Life Tables, 2017”, National Vital Statistics Reports, Vol. 68, No. 7, Centers for Disease Control and Prevention, June 24, 2019, Table A.