Last August, I wrote that when the Trump administration was encouraging illegal aliens to “self-deport”, it made absolutely no sense to keep Treasury regulations on the books that purposefully made it easier for illegal aliens to remain in the U.S. I urged that the misbegotten regulations, which should never have been promulgated in the first place, be repealed.

Then, last October, Sen. Tom Cotton (R-Ark.) sent a letter to Treasury Secretary Scott Bessent “urg[ing] the … Treasury to undertake a comprehensive review of current rules that allow illegal aliens to obtain financial services and access to the US banking system, including the regulations governing the acceptance of foreign identification documents for opening bank accounts” and “request[ing that Treasury] … explore whether [federal law] could appropriately be utilized to prevent illegal aliens from opening accounts at U.S. financial institutions”.

On Tuesday, President Trump issued an Executive Order — “Restoring Integrity to America’s Financial System” — in which he proclaimed that “My Administration will not … permit risks to our financial system posed by the extension of credit or financial services to the inadmissible and removable alien population.” Through the EO, President Trump has required Secretary Bessent to “consider changes to applicable implementing regulations … to strengthen risk-based customer identification program requirements … account[ing] for the risks foreign consular identification cards pose to the integrity of the United States financial system”.

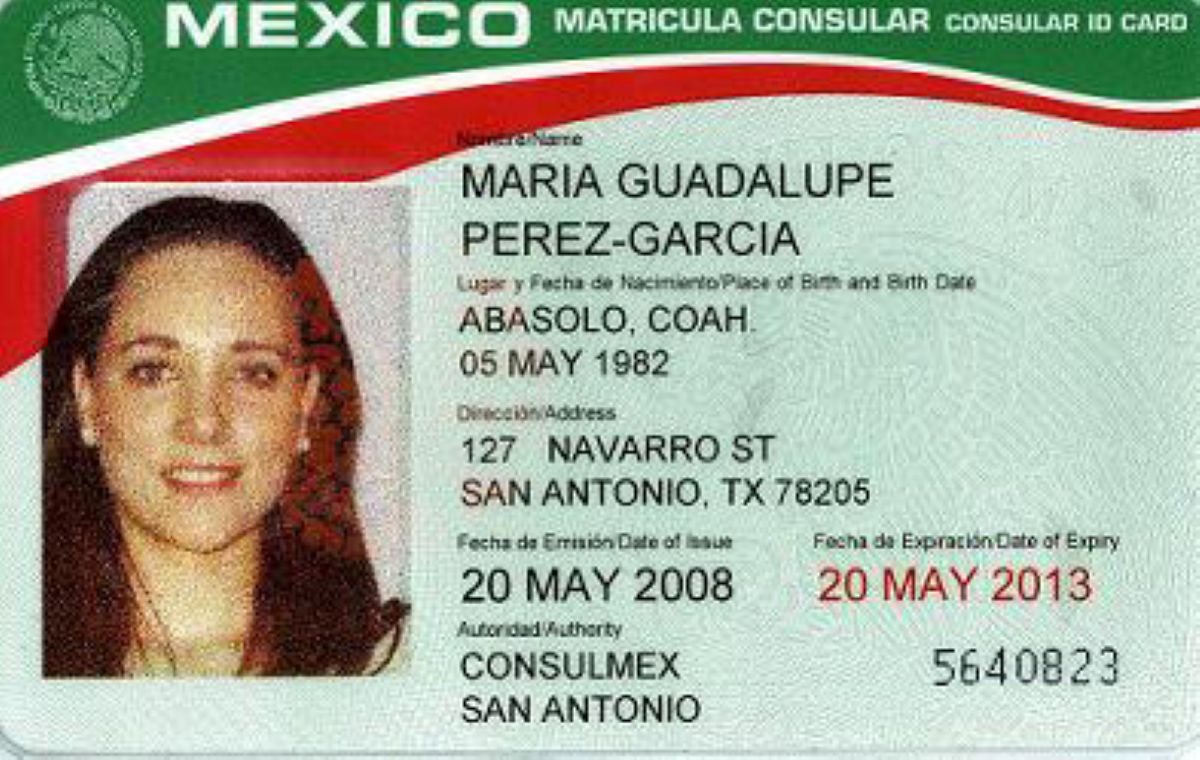

Mexican Matrícula Consular Cards

After the 9/11 terrorist attacks dashed Mexico’s and the Bush administration’s hopes for a mass amnesty for illegal aliens, the Mexican government turned to a strategy of persuading federal, state, and local governments and the U.S. banking industry to accept Mexico’s matrícula consular card for identification purposes for Mexican illegal aliens.

The matricula consular (Spanish for “consular registration”) card is an official ID issued by the Mexican government through its consulates to citizens living outside the country. Many countries issue such cards.

Mexico’s goal was to achieve a de facto amnesty by making it easier for illegal aliens to remain in the U.S., especially by receiving banking services. This would also safeguard the continued flow of remittances back to Mexico.

Mexico’s strategy was extraordinarily successful, facilitated by many U.S. banks’ desire to profit by turning millions of illegal aliens into customers: By the summer of 2003, more than 402 localities, 32 counties, 122 financial institutions, and 908 law enforcement agencies agreed to accept the matrícula for identification purposes.

The “USA PATRIOT Act”

The matrícula fiesta was momentarily threatened by enactment of the “USA PATRIOT Act” in October 2001. The Act required the Treasury to issue regulations “requir[ing] financial institutions to implement … reasonable procedures for … verifying the identity of any person seeking to open an account”, with the goal of “provid[ing] the United States government with new tools to combat the financing of terrorism and other financial crimes”.

The Treasury Regulations

But the regulations that the Treasury actually wrote turned Congress’s intent on its head. By their own words, they did “not discourage bank acceptance of the ‘matrícula consular’”. Why? The Treasury readily admitted that it was trying “to find a balance between the need for strong regulation that provides a real benefit to those working to achieve national security and law enforcement objectives and the ability of financial institutions to serve non-U.S. persons” and that it was worried that “efforts to deter money laundering and disrupt terrorist financing … might have a negative impact on … encourage[ing] … non-U.S. persons living and working in the United States [read: illegal aliens] to use mainstream financial services”.

I am sorry that “efforts to deter money laundering and disrupt terrorist financing” might have interfered with encouraging illegal aliens to use our banking system! These were not words written by President Obama’s Treasury — they were written by the Treasury of President George W. Bush, on whose watch the 9/11 terrorist attacks had occurred not long before.

Roger Waldinger, professor of sociology at UCLA and director of UCLA’s Center for the Study of International Migration, explained that once Treasury had published its proposed regulations, “As described by the American Banker [in an article titled ‘Foreign I.D. Ban Seen Damaging Immigrant Biz’] the banking industry went ‘on the offensive’ … , opposing any move to limit the [matrícula] card’s use. … Ultimately, Treasury decided not to recommend any further changes, much to the satisfaction of both banks and the Mexican government.”

As then House Judiciary Committee Chairman F. James Sensenbrenner, Jr. (R-Wisc.), wrote, “The intent of the Congress in directing the Treasury to write new regulations was to raise the bar on the difficulty with which terrorists can move money through the U.S. banking system. As written, the regulation appears instead to lower the bar.”

President Trump

In his new EO, President Trump requires Secretary Bessent to:

Issue a formal Advisory to financial institutions regarding the risks associated with the exploitation of the United States financial system by non-work authorized populations and their employers … describ[ing] specific red flags … associated with … categories of suspicious activity [including] … the use of an individual taxpayer identification number … to obtain credit products or open depository accounts where the applicant lacks verified lawful immigration status … [with the goal of] ensur[ing] the account is not being utilized to facilitate the unlawful employment of unauthorized aliens[;]

Propose changes to applicable implementing regulations … [to] ensure that … institutions maintain the authority … to obtain additional information … relevant to whether account holders possess lawful immigration status and employment authorization in the United States when such information is relevant to assessing risks associated with fraud, identity misrepresentation, sanctions evasion, or other illicit financial activity[; and]

Consider changes to applicable implementing regulations … [to] account for the risks foreign consular identification cards pose to the integrity of the United States financial system.

Additionally, through his EO, President Trump requires the Consumer Financial Protection Bureau to “consider clarifying that potential deportation and loss of wages are factors that could adversely affect a non-work authorized borrower’s ability to repay an extension of credit under the ‘ability-to-repay’ standards” and requires federal financial regulators to “issue guidance regarding the management of the potential credit risks posed by the non-work authorized population”.

June 9 will be the 23rd anniversary of the effective date of Treasury’s permissive regulations. President Trump has given us hope that those regulations will not see another one.