Download a PDF of this Backgrounder.

David North is a fellow at the Center for Immigration Studies. Donna Desrochers provided valuable research assistance.

One of the more obscure impacts of our immigration policies is on charter schools that provide K-12 education for what would usually be public-school children. The subject of this report is the handful of charter schools that have used EB-5 investments to get started.

It appears that the investors, the kids, the teachers, and the taxpayers are all in the same boat, contributing generous but unknown amounts of money to all the educational middlemen. And the middlemen are often trying to hide information on this situation.

Alien Investors. We will initially focus on how the alien investors in these programs are likely to be treated. Will the aliens, who will also get a set of green cards for their families, ever see their half-million-dollar investments again? If so, how long with it take before they are repaid?

Much public policy analysis is, without saying so, geared toward moneyed interests, the famous 1 percent. This study shows how one small subclass of the 1 percent — rich aliens who have invested in the EB-5 program and in the charter schools — is likely to be treated in the future.

One of the reasons we have taken this approach is that, unlike EB-5 programs generally (which usually fund glitzy real estate developments in prosperous urban areas, doing so in near total secrecy) there is a certain amount of public financial information on the EB-5 program's interactions with charter schools.

We found a list of 24 entities covering 25 charter schools that had EB-5 funding; there were financial reports available for 11 of the 24 and there were no financial reports available for 13 (some of the schools were very young). We examined the 11 with care, thinking in terms of the interests of the aliens and their investments.1

So what have been the financial consequences for these investors?

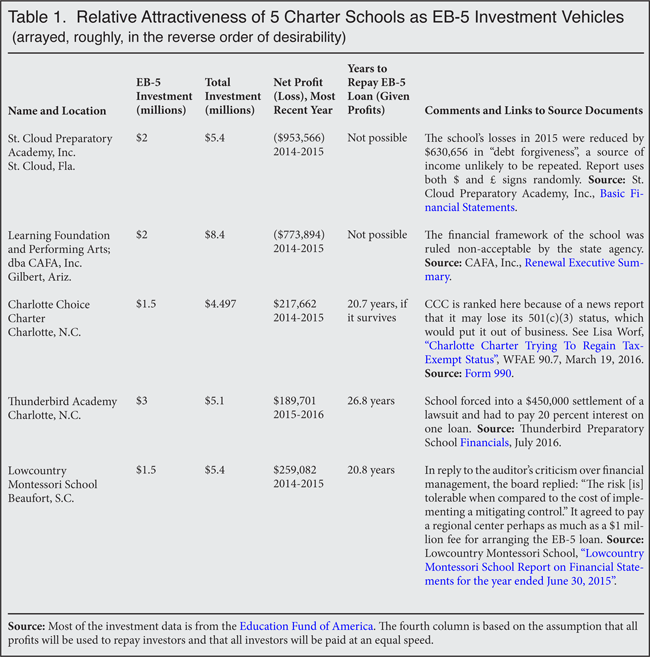

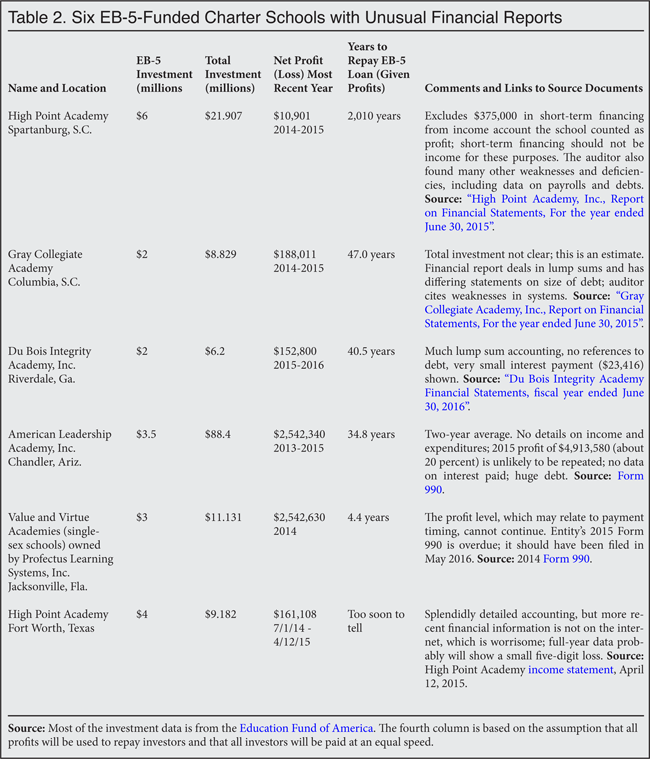

Glancing at the tables that follow, it is clear that most of the full repayments of the EB-5 loans, if they happen at all, will be decades in the future and that in the meantime the charter schools' collective financial returns, with a single exception, are a CPA's nightmare.

More specifically, there is an almost bizarre range of interim results of these investments, from several projects that seem doomed to early failure to one that is bringing obscene levels of profits to its managers (but probably not to its investors). That charter school, over a period of two years, showed that 45 percent of the public money it had received had been spent on education, and 55 percent on profits.

Investors should also know that, by definition, a charter school that wants EB-5 money has been unable to raise capital from the normal sources, and is thus more at risk than charter schools generally. Raising money through the EB-5 program is expensive and awkward. Peter Elkind, the senior Fortune writer who exposed the Enron scandal, made this point about EB-5 projects generally, writing:

But because the EB-5 industry is virtually unregulated, it has become a magnet for amateurs, pipe-dreamers, and charlatans, who see it as an easy way to score funding for ventures that banks would never touch.2

While any financial reporting on an EB-5 project is welcome, much of it in this set of 11 is opaque, some of it seems contrived (to use a gentle term), and in one instance it is splendid in its detail, but not in its completeness, since it covers less than a full year. And it should be borne in mind that there were no reports at all from 13 of the operations. There are no national norms for such reporting, and it shows.

In short, investors beware.

The Basics — EB-5. The EB-5 program (the fifth of the employment-based categories in the American immigration system) provides, in its most active operation, a family-sized set of green cards for an investor making a half-million-dollar investment in a Department of Homeland Security-recognized project. DHS, thank goodness, does not guarantee these projects.

Each project is supposed to be "at risk", i.e., there can be no guarantees of repayment; each is supposed to create 10 jobs. The investments are routinely pooled by the DHS-licensed regional centers. The program is controlled, to the extent that it is, by the U.S. Citizenship and Immigration Services, a DHS entity that has no other contact with high finance.

There is an upper limit, set by Congress, of 10,000 visas in the program, producing about 3,000 half-million-dollar investments a year. More than 90 percent of these visas are issued to nervous Chinese businessmen. We may assume that these aliens would not be able to secure immigrant visas in any other way, or they would not invest the money. Currently there is a multi-year backlog of visas for the Chinese, which gives the EB-5 middlemen an excuse for urging the expansion of the 10,000 limit.

In many cases the alien investors — far more interested in the set of visas than the fate of their investments — do not do much due diligence, and are thus easy targets for shaky and sometimes fraudulent schemes. To the EB-5 middlemen they are thus providers of a large pool of funds that are not only "patient" but also are passive, uninformed, and unlikely to seek redress.

The part of the EB-5 program being described here is due to expire on December 9, 2016. Congress seems likely to extend it again, probably for a year or two, and the question is: Will those who want to reform the program prevail, or will it be extended in its current form? Investments made prior to December 9 will continue to be honored whether or not the program is extended.

The Basics — Charter Schools. Whereas the EB-5 program is federal, the creation and funding of charter schools are subject only to state and local (school board) control, which is highly uneven. Thus there are no national standards and no national reporting requirements. Charter schools are popular with conservatives, as they seem to offer, like private prisons, a way to reduce the size of government.

Charter schools are 95-99 percent funded by tax funds and provide tuition-free education to K-12 students. Moneys used to support these schools come from board of education budgets; the funds would otherwise go to public schools. Generally, but not always, grants made to charter schools are made at the per capita rate used in the public schools. A minority of America's K-12 students attend these schools.

Some charter schools, like most in our study, are stand-alone entities. Others are parts of either acknowledged or unacknowledged chain operations. In the latter category are the schools operated by the followers of the Turkish imam Fettullah Gulen, about which we have written frequently.3 None of the 11 studied schools relate to the Gulen cult.

Defenders of the charter schools say that they allow for a more varied menu of educational choices than the public schools; for instance, one of the 11 studied entities follows the teachings of Maria Montessori and two others in the set (who share the same owner) are single-sex schools.

The EB-5/Charter Mix. While some states, such as South Carolina, demand that charter schools have section 501(c)(3) standing as IRS-recognized non-profits, all EB-5 moneys must go, by law, to at-risk, private-for-profit corporations. This creates a messy dynamic in which there must be both a for-profit and a non-profit entity for each charter school; this complicates financial reporting and ensures the largely unreported transfer of public moneys into private hands. (Typically, the non-profit arm pays rent to the for-profit arm, sometimes providing the latter with unreasonably large and hidden profits.)

The EB-5 funds in charter schools are routinely used to provide capital for the school buildings and, as we will see, the EB-5 role in financing is masked through rental payments. One of our reliable China-based informants provided this translation from an EB-5 offering in Mandarin on this point:

The real estate developer borrows money from the EB-5 investor partnership to finance the construction of the school. The EB-5 loan is guaranteed on the building and the land as well as the renting income.

The overstatement regarding the guarantee — there is no such guarantee to the investor, though there may be to the developer — is fairly typical of these proposals in Mandarin.4

Our Findings

We show in the two tables that follow the extent of the EB-5 debt and total debt of each of the 11 schools, the apparent profit for the most recent year of operation (a two-year average in one case), the expected number of years it will take at the profit level shown for the capital to be repaid, and notes on the apparent financial shape of the school and on some of the many quirks in the financial reporting.

In terms of the debt structure, all of the schools have both EB-5 and non-EB-5 financing. In all but one the EB-5 portion is for a minority of the debt. The EB-5 debts vary from $1.5 million to $6 million and the total debt loads from nearly $4.5 million to a thumping $88.4 million. Many of the financial statements do not even acknowledge the presence of any long-term debt.

In terms of prospective repayment of the EB-5 debt, it should be noted that this is a variable never discussed in any of these reports. These are our calculations based on the assumption that the current annual level of profit (or loss) will persist, that all profits will be devoted to debt repayment — a truly rosy assumption — and that all debts, EB-5 and other, will be paid off at the same rate of speed.

Generally, it will take a long time for these debts to be paid off, if that even happens, as it probably will not in several cases. There are four groupings:

- Schools that will either fail or, in one case, take more than 2,000 years to pay off the debt (St. Cloud, Learning Foundation, and High Point, S.C.);

- Schools that will be able to pay off their debts (given the assumptions) in 20 to 50 years. This is the largest group and includes these six schools: Charlotte Choice, Thunderbird Academy, Gray Collegiate, Du Bois, American Leadership, and Lowcountry Montessori. The average payoff time for these six is 31.8 years;

- One school without a full year's financial report (High Point Texas) and thus it is too early to tell; and

- One entity (which covers the Virtue and Valor Academies) with a 55 percent profit rate is unlikely to be able to sustain that rate of profit. If it can do that, it could pay off the EB-5 loan in 4.4 years.

Then there is the variable of the interest paid. In only one instance was that reported, and that's the 1 percent rate shown in the Lowcountry Montessori report. Few of the reports show more than small amounts of interest paid, so we can safely assume that the thrust of the Lowcountry report — that interest payments are buried in the lease payments — probably is universal. One percent interest, which we have seen in many non-charter school EB-5 situations, is probably the norm, and it may be the maximum.

In summary, the financial reports are grim from the investor's view. He may not be repaid at all, if paid in full it probably will take something like 30 years, and there will probably be interest payments at the rate of 1 percent a year. Without the visas there would be absolutely no market for such feeble returns on investment.

Bear in mind that the financial reports summarized in Table 1 are the better ones in the set of 11; when there are problems, they are largely visible ones.

The financial reports discussed in Table 2, to my non-CPA's eyes, seem to be more troublesome and less transparent than the ones in Table 1. In a couple of cases more recent financial reports should be available than those shown, which, in itself, is a worrying sign.

Quality of the Financial Reporting

With the single exception of the document filed by the High Point Academy in Texas, the quality of the financial accounts is disappointing. In addition to the apparently general practice of hiding the interest payments on debt in the leasing category, and the frequent non-acknowledgment of long-term debt, we found these problems:

- Much lump sum reporting, which hides useful information; in one extreme case, that of the American Leadership Academy, there are just two expenditure items shown: administration: $1,285,405, and instruction and operations: $20,023,283;

- Three of the statements were in IRS forms 990, essentially the income tax returns of non-profit entities; in none of these was the requested data on the salaries of executives shown (American Leadership, Charlotte Choice Charter, and Profectus Learning Systems);

- There were several just plain odd entries, such as in Thunderbird Academy's report on expenditures, which included: -$3,915, archery expense, and -$1,066 insurance expense, suggesting that these were income items; puzzling; and

- There was the written statement by Lowcountry Montessori that it simply would not devote resources to do what was needed to improve its financial reports5

It could be argued that the schools need not show the long-term debt because that relates to the linked for-profit entity that owns the land and the buildings. That might be narrowly correct, but it would be a sleight-of-hand inappropriate in an accounting of public funds.

In short, if the investors were to engage in due diligence — or more significantly, were the school districts to do so — they would find it difficult, in most cases, to see the true financial picture of these schools.

Impacts on Children, Teachers, and Taxpayers

Let's turn away from the impact of the EB-5/charter school combination on the 61 alien investors (who put up a total of $30.5 million) and discuss the impact of this arrangement on thousands of children, hundreds of teachers, and a much larger number of taxpayers.

The big picture is that dollars spent on profits and fees to the regional centers handling the 61 investments is money that would be spent on kids and teachers were they all in the public school system. We will never know how much was siphoned off in this way in these 11 schools because of the financial reporting, but it is safe to say that many millions are involved. Similarly, taxpayers, instead of knowing that all their tax dollars are going to the schools, must accept that some of these dollars are heading into private hands instead.

The lack of detail also means that we do not know, but worry about, the salary levels of the teachers in these schools, as opposed to salaries in the public schools. In many cases, for instance, we do not know if the teachers are getting the fringe benefits that typically accompany work in the public schools, such as the employers' payments of Social Security, Medicare, and unemployment insurance, as well as pensions. (These payments are made in the case of High Point Academy in Texas, however, and probably in some of the others.)

Postscript

I read the internet statements made by immigration-related educational institutions very carefully these days, after finding one in which the word "interest" was spelled four different ways in five lines of type.6 While the Education Fund of America (EFF), which specializes in EB-5 and charter schools and whose data we have used, does not reach those heights, contemplate the following from its website:

The Kaufman Foundation study ... showed that on average 399 out of more than 400 charter schools payed off all their facility financing. This is a 99.76 percent success rate. 7

Set aside the question of the likelihood that anything in the charter school business — or life in general — would be that successful.

Ignore the archaic "payed" for the moment.

Forget the incorrect spelling of the foundation (it should be Kauffman).

Let's look at the math.

Clearly 399 out of 400 is 99.75 percent, but EFA writes that 399 out of more than 400 is 99.76 percent. Intrigued, I tried 399 out of 401 and got 99.50 percent, and then 399 out of 402 and got 99.25 percent; so either the 399 is a rounded number, or the 400 is, or maybe both. The real number is not shared with us. Or maybe something else is wrong.

Enough with concepts, and words, and numbers, maybe these people draw really, really nice pictures.

End Notes

1 See the Education Fund of America website.

2 See Peter Elkind and Marty Jones, "The dark, disturbing world of the visa-for-sale program", Fortune, July 24, 2014.

3 See David North "Los Angeles Terminates Three Gulen Schools for Hiring Turkish H-1B Teachers", Center for Immigration Studies blog, October 19, 2016.

4 The full 51-page prospectus in English and Mandarin, from an entity whose name is not translated, regarding EB-5 and charter schools in Florida can be seen here.

5 See David North, "S.C. Tax Money Meant for Kids and Teachers is Sent to Distant Middleman", Center for Immigration Studies blog, October 26, 2016.

6 See David North, "Should a School with a Financial Statement Like This Be Authorized to Teach Accounting to Foreign Students", Center for Immigration Studies blog, August 5, 2014.

7 See the Education Fund of America's page on its Charter School Investment Fund.